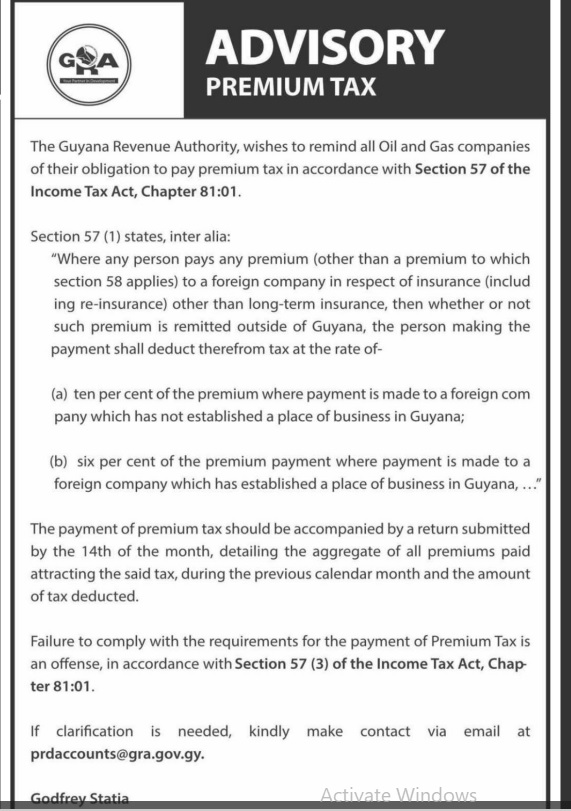

In a recent advisory, the Guyana Revenue Authority (GRA) has issued a reminder to all Oil and Gas companies regarding their obligation to pay premium tax as stipulated by Section 57 of the Income Tax Act, Chapter 81:01.

Under Guyana’s production sharing agreement, which encompasses billions of dollars in exemptions, there exists a contention provision that warrants attention. This provision allows oil-producing companies to essentially have Guyana pay their taxes out of the country’s share of profits earned. Additionally, the provision exempts foreign producers from paying taxes in their country of origin.

According to Section 57(1) of the Act, companies are required to deduct tax from any premium paid to a foreign company for insurance, excluding long-term insurance. The deduction rates are specified as follows:

Ten percent of the premium is paid to a foreign company without a place of business in Guyana.

Six percent of the premium is paid to a foreign company with an established place of business in Guyana.

According to the tax authority, it is imperative that the payment of premium tax is accompanied by a detailed return, which must be submitted no later than the 14th of each month. This return should outline the total premiums paid, subject to the tax, during the previous calendar month, along with the corresponding amount of tax deducted.

Failure to adhere to these requirements constitutes an offense under Section 57(3) of the Income Tax Act, Chapter 81:01, according to GRA.

{kind=link}